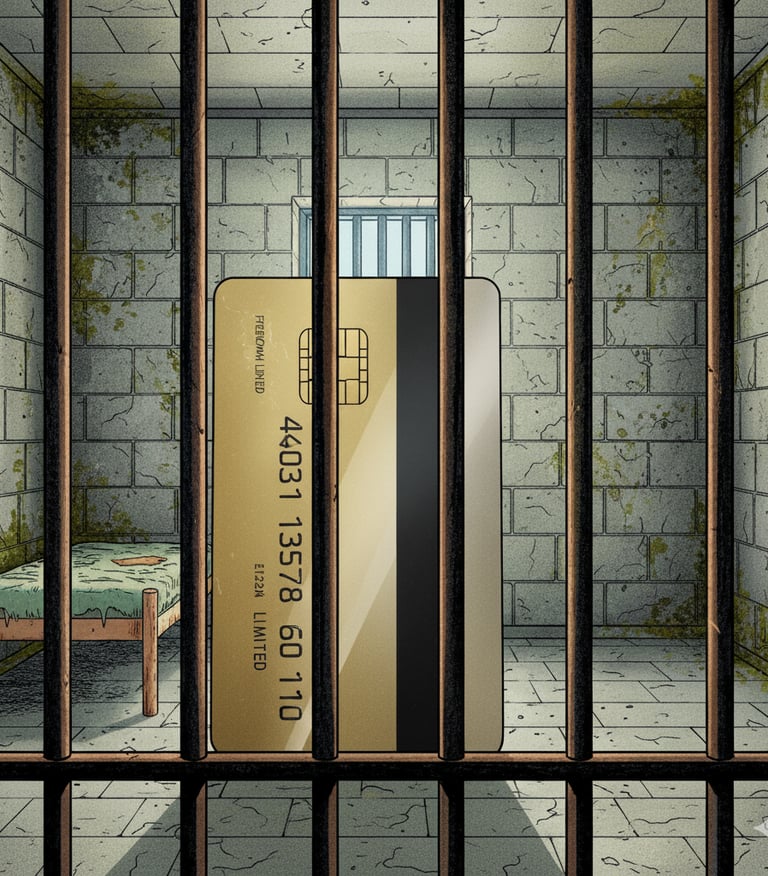

Chase Killed the INK Train. Did Travel Blogs Get Us Here?

Another day and another sad trombone update from Chase. Has me wondering, "You Okay, Chase?" and also wondering if travel blogs got us here.

11/22/20254 min read

It’s the daily bad news for churners from Chase

Fresh off yesterday’s post about Chase’s new restrictions on sign-up bonuses for their fee-free INK business cards (INK Cash and INK Unlimited), there’s more bad news for churners: Chase’s fee-based INK business Preferred card ($95 annual fee) now has once per lifetime language (Source: Doctor of Credit). These restrictions apply retroactively. For longtime churners, this is an abrupt stop.

Got the bonus three years ago? You may be locked out forever. It’s not a 4 year reset, or a 7 year reset; it’s lifetime limited. The word 'may' in 'may not be available' leaves the door cracked open—maybe Chase will reset these after 7 years like Amex reportedly does. But I wouldn't count on it. The Chase INK train has grounded to a halt, last stop, all disembark.

Let’s recap: Since June 2025, Chase has tightened up bonus restrictions by:

Adding lifetime language to sign-up bonuses for their Sapphire cards (the $95 preferred and the $795 reserve). Previously it was a 48 month reset.

Creating “family rule” limitations to the Sapphire cards, so a previous bonus on a Sapphire Preferred means that you will not get one on a Sapphire Reserve, and vice versa.

Reducing the referral points awarded for Chase INK cards from 40,000 to 20,000

Limiting the ability to earn referral points to only applicants who have not ever had a Chase INK card before (this really hurt if you were in Two Player mode).

Added once-per lifetime sign-up bonus language to the fee-free Chase INK cards (INK cash and INK unlimited), and created a “family” for these two cards so it’s one bonus, ever for these two cards.

And the most recent news about once-per lifetime language on the INK Preferred

Let me know if I missed something in the comments.

What does this all mean? (primer for beginners)

Lifetime language is when credit card companies put restrictions on how often you can receive a sign-up bonus. The most restrictive is “once in a lifetime” (🎵This is not my beautiful sign-up bonus 🎵); which means this is a one and done sign-up bonus. It is the antithesis of churning which is the strategy of opening and closing the same card repeatedly to harvest multiple bonuses.

Card families are when banks group similar cards together and say "pick one bonus, not both." Get a bonus on one card in the family, and the siblings are off-limits.

Here's how Chase's INK families break down:

No-fee family: Ink Cash and Ink Unlimited = one bonus total between them

Annual-fee card: Ink Preferred = separate bonus (for now)

So you can get one bonus from the no-fee family AND one bonus from the Ink Preferred. After that, you're done with Chase Ink bonuses.

Pop-up jail is when you're filling out a credit card application and a message appears saying essentially: "You can apply, but you won't get the sign-up bonus which, let's be real, is the only reason you are doing this." AMEX pioneered this move, and now Chase is using it too. The upside? At least you know before the hard credit pull.

Does this matter to you?

If you have never had a Chase INK business card, then you can still apply and receive a sign-up bonus. Nothing has changed there, but if you read about the INK train on any old posts on travel blogs, know that this train has left the station.

If you woke up today and learned that you already used up your lifetime opportunities for bonuses, well this does necessitate a change in card strategy and possibly, your points spend.

“Chase, you okay?”

Once again I wonder, "Chase, you okay?" So many money-saving moves can rattle consumer confidence. Maybe these restrictions say less about churners and more about Chase's bigger financial picture. Maybe they're preparing for economic uncertainty. Maybe the Sapphire lounges really did blow the budget. Maybe the marketing department overspent on last summer's ad blitz for the Chase Sapphire Reserve refresh. Or maybe—and this feels most likely—they realized they were paying out more in bonuses than they were making back in interchange fees and interest.

Whatever's driving this, Chase is releasing new restrictions almost daily. It's erratic. Time to panic? I’m not sure. Sometimes you just have to let the toddler burn through the tantrum and see where things settle.

Any upsides to these changes?

I found only two:

I do appreciate the clarity of the pop-up jail and I’d much rather know if I wasn’t going to get a bonus before getting a hard-pull on my credit report.

Does 5/24* even matter anymore? If Chase bonuses aren't worth chasing anymore, why worry about staying under 5/24 for them?

That’s the thin silver lining.

Did the Points and Miles Influencers derail the INK Train?

Here's the question I can't stop thinking about: How much of this is on the influencers who spent years telling everyone "Start with Chase"? When every major blog pushes the exact same cards to millions of readers, is it any wonder Chase noticed? The INK train didn't just slow down; it got so crowded that Chase kicked everyone off.

I'm not exempt from this either. Even as a new blog, I'm part of the ecosystem. But maybe the lesson here is that the next time every blog is pushing the same "hack," that's exactly when to be skeptical. The best opportunities are rarely the ones everyone's shouting about. And maybe we all need to slow down and think instead of racing to apply before the next restriction drops.

So what's next? I'm still figuring that out. What about you?

*5/24 is Chase’s unwritten rule that you can only have five personal credit cards from any bank in a 24 month period; exceed that and you will not get any approvals.